Isabelle a hérité d’une partie de l’entreprise de sa famille à l’âge de 19 ans – voici comment elle s’y est prise pour se préparer en vue de l’avenir.

Isabelle Inherited Part of the Family Business at 19 — Here’s How She’s Set Herself Up for the Future.

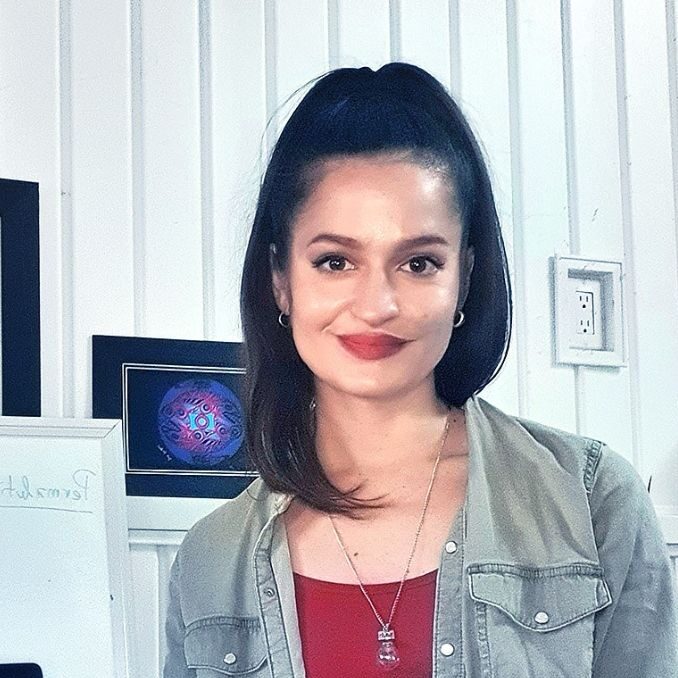

Andrea Casciato embraced change throughout her career — now she’s the Head of Digital Investing with BMO.

These food entrepreneurs went from their kitchen to national grocers while focusing on nutrition and sustainability.

Canada’s first zero-waste grocery store founder offers simple tips to make your shopping more eco-friendly.